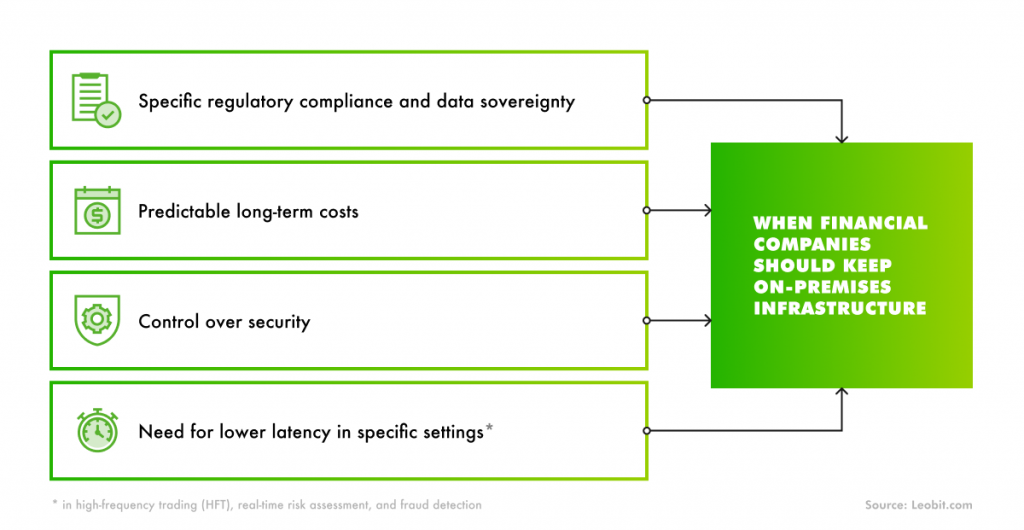

Fintech firms, banks, and financial service providers manage vast amounts of sensitive financial data, which makes security and regulatory compliance a must. However, as financial regulations become more stringent, companies face growing challenges in ensuring compliance with frameworks, including the following:

- Banking regulations. Banks and credit institutions must comply with Basel III, GDPR (for EU operations), and the Bank Secrecy Act (BSA). These require stringent risk management, customer data protection, and anti-money laundering (AML) practices.

- Securities and investments. Firms dealing with trading, brokerage, and investment services need to adhere to SEC, FINRA, and MiFID II (for European markets) guidelines, ensuring transparency, data integrity, and fraud prevention.

- Payments and fintech compliance. Payment processors and digital lenders must comply with PCI DSS for transaction security, while fintech firms handling cryptocurrencies or digital assets fall under FinCEN’s AML/KYC regulations.

With on-premises infrastructure, companies bear full responsibility for ensuring compliance, monitoring threats, and updating security measures to align with evolving regulations. This includes:

- Implementing encryption and data access policies

- Maintaining and auditing security controls

- Ensuring real-time threat detection and incident response

- Keeping up with ever-changing regulatory updates

- Disaster recovery and data back-ups

This is a significant burden, which requires a dedicated team and ongoing investments in security tools and expertise.

Can cloud ease this burden?

Big cloud providers like Azure or AWS offer built-in security and compliance frameworks. So, unlike on-premises solutions, where companies handle everything internally, cloud adoption follows a shared responsibility model where a cloud provider continuously monitors compliance requirements and implements updates to meet industry standards (e.g., SOC 2, ISO 27001, PCI DSS, GDPR).

The financial company’s responsibility lies in configuring security policies, controlling access, and managing application-level security. The cloud offers pre-configured compliance tools, automated monitoring, and real-time reporting, simplifying audits and reducing regulatory risk.

The cloud also offers advanced security features like zero-trust verification, encryption, pre-configured compliance tools, automated monitoring, and real-time reporting, which can boost security, simplify audits and reduce regulatory risk. According to the Cloud Security Alliance reports 57% of organizations already store or process regulated banking information within cloud services. No surprise since built-in compliance features simplify adherence to regulatory standards and help your company remain audit-ready.